Before you write your resignation letter, run the numbers. The clock is already ticking—and the bill for Year 1 was set the moment your last JTC paycheck cleared.

For many foreign engineers transitioning from a JTC (Traditional Japanese Company) to freelance, achieving higher pay is the ultimate goal. However, many are blindsided by a massive “Year 1 NHI Shock”—where your first health insurance bill, based on your previous salary, completely disrupts your cash flow.

Most engineers assume they can fix this after they resign. They cannot. Blue Return (Aoiro Shinkoku) is a powerful weapon—but it only works on income you earn as a freelancer. It cannot touch the bill that’s already been calculated from your JTC salary. That damage is done the moment you walk out the door.

Simulating your real take-home pay before you resign is critical, not after.

In this guide, we break down the social security logic most engineers miss and hand you a Japan National Health Insurance Calculator — also known as a Shakai Hoken calculator for those transitioning out of corporate coverage — to stress-test your numbers today.

Contents

- 1 Interactive NHI Simulator: Calculate Your Year 1 Freelance Cost

- 2 Japan Health Insurance Cost: The “Year 1 Shock” Before You Resign

- 3 The Four-Stage Reality of Leaving Your JTC

- 4 The Ghost in Your Bank Account: You’ll Spend Year 1 Paying for Someone You No Longer Are

- 5 Freelance Tax Japan: What You Can’t Change After Resigning

- 6 Shakai Hoken vs. NHI: Why Freelance Premiums Skyrocket

- 7 The Hidden Costs: How JTCs Subsidize Your Social Security

- 8 Beyond the JTC Safety Net: Understanding Japan’s National Health Insurance

- 9 Maximizing Your Medical Tax Deduction and Insurance Tax Return

- 10 Conclusion: The Simulation Shows the Damage. Act Before It’s Final

- 11 Next Steps: Level Up Your Navigation

Interactive NHI Simulator: Calculate Your Year 1 Freelance Cost

Don’t rely on intuition—use data to project your first year as a freelancer. This Japan health insurance calculator goes beyond simple premiums — unlike a basic NHI calculator, it simulates your true take-home pay by factoring in both NHI costs and the impact of Blue Return tax optimization.

Run your diagnostic below. The number that appears is not a projection—it is already decided.

Run your diagnostic below to see your real numbers before making the leap.

How to Use the Simulator

- Enter Previous Year’s JTC Income: Input your gross annual salary from your last year at the JTC. This is the figure that determines your Year-1 National Health Insurance premiums—even if your freelance income is different.

- Input Projected Freelance Revenue: Specify your target annual gross sales as an independent engineer. This helps calculate your true take-home pay after all deductions.

- Set Monthly Expenses & Family Size: Enter your estimated monthly business costs (servers, hardware, software licenses, internet). Then specify the number of family members—NHI charges a per-capita levy for each person, unlike corporate Shakai Hoken which covers dependents for free. Check the “Age 40+” box if applicable, as Nursing Care Insurance adds an additional premium.

- Review Results and Decide Your Next Action: The results screen shows a comparison of your JTC take-home vs. freelance take-home, your Year 1 NHI burden, the resident tax time-lag impact, and your tax-saving potential. The Go/No-Go indicator uses three tiers (🟢 Safe / 🟡 Caution / 🔴 High Risk). Read the results with this question in mind: “What can I still do before I resign to reduce these numbers?” If you see 🔴, pre-resignation optimization is especially critical.

How Japan National Health Insurance Calculation Works: 5 Costs Freelancers Miss

This simulator is built on five critical calculation layers tailored for foreign engineers transitioning from JTC employment to freelance status in Japan as of 2026. It does not merely estimate premiums—it simultaneously calculates five cost factors that directly affect your post-resignation cash flow.

Layer 1 — National Health Insurance Premiums (~10.5% + Per-Capita Levy): Unlike corporate Shakai Hoken where your employer covers 50%, freelancers bear the full burden. Critically, these premiums are calculated on your previous year’s income—meaning your first year’s bill is a direct inheritance from your JTC days. No amount of Blue Return optimization can reduce a bill calculated on income you earned as an employee. A per-capita levy of approximately ¥52,000 is added for each family member.The 2026 Child and Childcare Support Levy (0.23%) is also incorporated. The annual premium cap is ¥1,060,000.

Layer 2 — Business Expense Deductions (Non-Taxable Threshold): As a freelancer, business expenses (servers, software, internet fees, etc.) are deducted from revenue to compress your taxable income. While salaried employees receive an automatic Salary Income Deduction (2026 table, minimum guaranteed ¥740,000), freelancers must track actual costs themselves.

Layer 3 — Income Tax (Progressive Rate / 2026 Updated Brackets): The 2026 tax reform raised the basic deduction to ¥1,040,000 (the so-called “¥1.78M wall” response). This simulator applies the latest brackets (5%–45%) to both your JTC period and your freelance period to accurately calculate the change in income tax.

Layer 4 — Resident Tax “18-Month Time Lag”: This is the trap many engineers overlook. Resident tax is assessed on the prior year’s income and billed the following year. In your first year of freelancing, you will be billed for resident tax based on your high JTC salary (prior year’s income × 10% + flat levy ¥5,000). This is the source of the “Year 2 Shock”—a sudden bill that arrives just as your freelance income is beginning to stabilize.

Layer 5 — Monthly Take-Home Break-Even Point (Go/No-Go Indicator): After subtracting all four costs above, the simulator calculates your true monthly take-home pay and compares it against your JTC take-home. The three-tier assessment:

- 🟢 SAFE (120%+ of JTC take-home) — Favorable conditions for going independent

- 🟡 CAUTION (100–120% of JTC take-home) — Pre-resignation optimization can improve your position

- 🔴 HIGH RISK (Below JTC take-home) — Pre-resignation action is strongly recommended

The “Tax-Saving Potential” shown in the simulator results reflects the expected reduction (up to 40% of NHI, capped at ¥420,000) if you execute the NIS-2026-R1 strategies. Use this figure to make your final go/no-go decision before resigning.

Japan Health Insurance Cost: The “Year 1 Shock” Before You Resign

The numbers you see in the simulator above are often higher than expected. This is because your Japan health insurance cost in Year 1 is an “inherited debt” from your JTC salary.

Most engineers assume their freelance tax strategy starts on Day 1. In reality, you spend your first year paying for the person you no longer are. Understanding this Year 1 Shock is critical to managing your cash flow before the first bill arrives.

The Four-Stage Reality of Leaving Your JTC

Stage 1 — SHOCK: Your Year 1 NHI is already decided. Your first health insurance bill as a freelancer has nothing to do with how well your business performs. It was calculated the moment your last JTC salary was processed. The simulator above shows you exactly how large that inherited debt is.

Stage 2 — THE TRAP: “I’ll optimize after I resign” is the most expensive mistake. Blue Return, iDeCo, and Furusato Nozei are all tools that work on income you earn going forward. They have zero retroactive effect on the Year 1 NHI bill. Believing otherwise is the trap that costs engineers ¥500,000+ in avoidable losses.

Stage 3 — THE ONLY WINDOW: Act while you’re still an employee. There is exactly one moment when you can reduce the Year 1 bill: right now, before you resign. Maximizing your social insurance deductions, registering overseas dependents, and optimizing your Furusato Nozei ceiling while you’re still on JTC payroll directly lowers the income figure that will haunt you in Year 1.

Stage 4 — ACTION: Quantify your risk, then close the gap. The simulator above shows you the “Year 1 inherited cost” that is already locked in. But where does that number actually come from? Here’s the mechanism behind it.

The Ghost in Your Bank Account: You’ll Spend Year 1 Paying for Someone You No Longer Are

Now you’ve seen the number. Here’s where it comes from.

During your entire first year as a freelancer, you will not be taxed as a freelancer. You will be taxed as the JTC employee you used to be.

Your National Health Insurance premiums for Year 1 are calculated from your previous year’s JTC income—a number that’s already locked in. No matter how little you earn in your first freelance year, that ghost salary follows you.

The only way to shrink that ghost is to act while you’re still an employee. Once you resign, the number is frozen. This is the window that closes the moment you submit your resignation.

Freelance Tax Japan: What You Can’t Change After Resigning

Now that you’ve seen your numbers, understand what is permanently fixed the moment you resign:

• Year 1 NHI premiums — Locked to your final JTC salary. Blue Return cannot reduce this.

• Resident Tax (the time-lag trap) — Calculated on the prior year’s income, the bill arrives up to 18 months after you earned it. It hits your bank account right when a raise or job change made you feel financially comfortable—a delayed, high invoice striking at the worst moment.

• Social insurance deductions taken while employed — The window to maximize these is only open while you’re on payroll.

• Furusato Nozei ceiling — Your JTC salary sets a higher donation cap than your early freelance income will. Once you leave, that ceiling drops.

• Non-resident dependent registration — Documentation requirements for overseas family members must be established during employment. One missed step voids the entire ¥380,000 deduction.

Failing to optimize these before resignation can cost you ¥500,000–¥1,000,000+ in preventable lifetime tax losses.

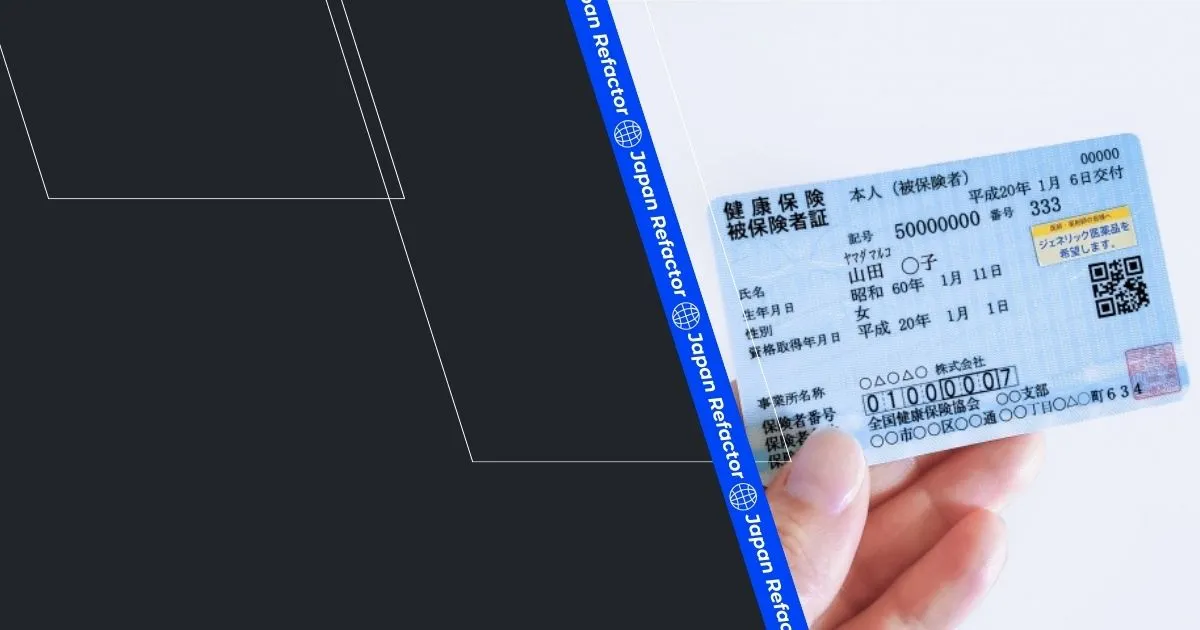

Shakai Hoken vs. NHI: Why Freelance Premiums Skyrocket

While working at a JTC, you are protected by the “Shakai Hoken” system. Many engineers search for a Shakai Hoken calculator when planning their transition — but once you go freelance, you automatically migrate to a system called “Kokuho” (National Health Insurance), and the calculation logic changes entirely.

Many engineers are shocked when their Health insurance premiums skyrocket during their first year of independence. This happens because these premiums are calculated based on your “previous year’s income.” Engineers who earned a high salary at a JTC often face formidable insurance costs immediately after resigning.

What makes this especially dangerous is the time lag: you have no ability to negotiate, delay, or reduce this bill after the fact. It is a fixed liability—a structural feature of Japan’s tax system, not a bug you can patch after deployment.

The Hidden Costs: How JTCs Subsidize Your Social Security

Why didn’t you feel the weight of these costs during your time at a JTC? It’s because the company was “under the hood” subsidizing about 50% of your premiums (the employer-employee split).

Going freelance means pulling the plug on this corporate subsidy. Costs that were previously handled in the background suddenly become visible, and 100% of the burden is withdrawn directly from your bank account.

Worse, National health insurance has no “dependent” system ; if you have a spouse or children, “per-capita” premiums are added for every family member. You must account for these hidden costs before making the leap. (For a more foundational overview of taxes and insurance, please refer to our “Japan Income Tax & Health Insurance 2026“.)

Beyond the JTC Safety Net: Understanding Japan’s National Health Insurance

Japan’s health insurance system is divided into two primary structures: one for corporate employees and one for freelancers or the self-employed.

According to Japan’s Ministry of Health, Labour and Welfare, the public system mainly consists of Employee Health Insurance (Shakai Hoken) and National Health Insurance (Kokumin Kenko Hoken). Please see “Japan’s National Health Insurance System” for further details.

Failing to understand the differences in this National health insurance structure before going independent can lead to critical errors in your financial cash flow.

The Ultimate Net Income Calculator for Japan-Based Software Engineers

Using a Net income calculator to determine your “true profit”—after subtracting income tax, residence tax, and high health insurance costs from your gross sales—is a mandatory task.

However, the calculator only shows you the damage. It cannot reverse it. The simulation above gives you the exact cost of your current JTC salary trajectory—the number that will follow you into Year 1. The question is not whether you understand the number. The question is: what will you do about it before you resign?

Ward-Specific Factors: Why Your Prefecture Affects Your Premiums

There is a key variable to watch when running your simulation: your local municipality. Since National health insurance is managed by local governments, tax rates and calculation coefficients vary by location.

For example, two engineers earning the same ¥8M salary could see a premium difference of over ¥100,000 per year depending on whether they live in central Tokyo or a suburban city like Saitama.

When using a Japan health insurance calculator or Japan national health insurance premium calculator, ensure you reference values that reflect your specific area of residence.

Maximizing Your Medical Tax Deduction and Insurance Tax Return

Understanding freelance tax Japan rules and using a reliable Japan national health insurance calculator are two essential steps for anyone planning to leave a JTC and work independently.

However, optimization has a deadline. Here is the honest framework:

BEFORE RESIGNATION (The Only Window):

- Maximize social insurance deductions on your final JTC paychecks

- Register and document non-resident dependents (¥380,000 deduction per person)

- Maximize Furusato Nozei contributions under your higher JTC income ceiling

- Verify your final salary figure and model the Year 1 NHI impact precisely

AFTER RESIGNATION (Year 2 and Beyond):

- Blue Return (Aoiro Shinkoku) — activates for your freelance income

- iDeCo contributions — begins reducing your ongoing taxable income

- Business expense tracking — servers, software, internet fees compress your future tax base

The engineers who thrive in Year 1 are not the ones who file the best tax return. They are the ones who optimized their last six months inside the JTC.

How Blue Return Deductions Lower Both Your Tax and Health Insurance Premiums

As the simulator above demonstrated, the Blue Return Deduction (Aoiro Shinkoku) is the single most impactful optimization for Year 2 and beyond.

Here’s exactly how to activate it—and when it actually takes effect.

This deduction system is defined by Japan’s National Tax Agency.

The brilliance of the Blue Return is that it reduces your “taxable income” by 650,000 yen, which fundamentally lowers the baseline for your Health insurance premiums, as well as your income and residence taxes. This means your Year 2 NHI premiums—calculated on your first-year freelance income—will be significantly lower. But this timeline also reveals the trap: it takes a full year of proper freelance filing before you see the benefit. Year 1 is already written.

While double-entry bookkeeping may seem complex, cloud accounting software like “freee” or “Money Forward” can automate the process via API links with your bank and credit cards—a concept familiar to any engineer.

Legally Minimizing Taxable Income to Escape the JTC Salary Trap

In the JTC world, “increasing your salary” was the metric for wealth. In the freelance world, the focus shifts to “maximizing your post-tax take-home pay.”

By accurately recording business expenses (cloud server costs, software licenses, hardware, internet fees, etc.), you can legally minimize (compress) your taxable income. When your income is compressed, your National health insurance premiums decrease accordingly. If you need professional advice in English regarding freelance tax Japan or optimal expense reporting, consulting with an English-speaking tax professional can be a highly effective move.

But these tools only work on income you have yet to earn. The damage from your JTC salary is already baked in. Start these habits on Day 1 of freelancing—and use the window before you resign to handle the Year 1 variables that can actually still be moved.

Conclusion: The Simulation Shows the Damage. Act Before It’s Final

An accurate pre-independence simulation prevents a “financial crash” in your career. Leaving the safe environment of a JTC is a fantastic challenge, but you should carefully simulate your finances before making the transition.

The simulation above does not show you a future you can change after you resign. It shows you the cost of your current trajectory—a number that will be permanently locked in the moment you submit your resignation letter.

Blue Return will protect your Year 2 income. iDeCo will compound over decades. But neither can rewind the clock on Year 1.

The window to change that number is still open—but only while you remain employed.

Action Step: Run a Simulation on our National Health Insurance Calculator Today

If you are currently a JTC employee planning to go freelance, your first action isn’t writing code or a resignation letter.

It is running the simulator above, looking at the Year 1 cost, and asking yourself: “Have I done everything I can to lower this number before I resign?”

As the simulator above revealed, the reality of National health insurance can be sobering. Review your results, adjust your projected revenue if needed, and set your personal go/no-go threshold.

If the results show that your Year 1 costs are higher than you expected—and you haven’t yet taken the pre-resignation optimization steps described above—the Net Income Shield (NIS-2026-R1) provides the exact playbook: what to do, in what order, before your last day at the JTC.

Only once you are confident you can maintain your lifestyle after paying those premiums should you seriously consider submitting your resignation.

And if the number concerns you—don’t wait. The window doesn’t stay open.

Get the exact bilingual scripts and documentation steps to lower your Year 1 bill.

This article is a sub-module of Layer 3. To master the complete career optimization protocol or explore the entire blueprint, choose your next destination:

🔼 Back to Layer 3: Career Strategy & Hacking Seniority (Return to the module overview: Salary Negotiation, Visa Hacks, and Promotion Logic)

🏠 Return to The Engineer’s Blueprint: Decoding Japanese Workplace Culture (Access the Master Manual including Genba Communication, Tech Specs, and Business Etiquette)

📥 DOWNLOAD IT FOR FREE